3rd March 2026

Essential (European) Kit Remote Workers Need in 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

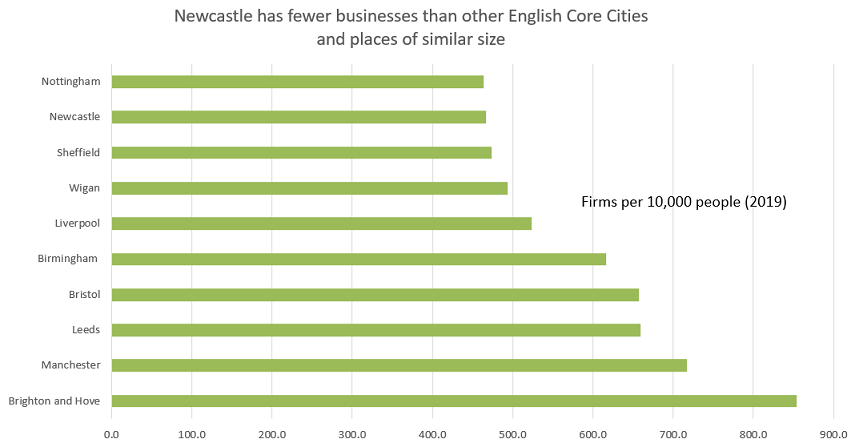

Read More >We have a great bakery in our part of town. We have a Greggs also – equally great, just different. In the former, I can buy a tremendous fruit loaf and their croissants are great too. But, for those who don’t live close to me, their choice is confined to Greggs. If I were to live in Brighton, it would be very different. We need more businesses in Newcastle to deliver jobs, GDP – and many more cakes.

Why can I taste the smell of bread, floating on the air in Brighton? It’s because there are more bakeries pumping their wares through the Sussex suburbs.

Put crudely, there are probably close to twice as many bakeries in Brighton as Newcastle. I’ve picked Brighton because the population is roughly the same size as that of Newcastle, even though it’s a seaside town and the business mix will be very different. If I abandoned population size as a constraint and stick with suburban places, then comparison with other South East locations suggests greater difference. For every one bakery in Newcastle, there will be 2.5 in Sevenoaks, Winchester and High Wycombe.

The chart shows how many businesses there are in Newcastle (per 10,000 people) by comparison with other cities. The differences are considerable.

There are 2 reasons why the number of businesses in a place is important.

It is a crude concept, but the reason that I cannot secure excellent patisserie across Newcastle is that there are too few bakeries. Therefore, there is little incentive to create scrumptious cakes. Or let me bring this closer to my own experience. (In spite of my example, I’m not a frequent consumer of cakes).

When we were developing The Racquets Court, we tried hard to place small contracts locally. These captured things like furniture, phones, internal switching gear and so on.

We failed.

There were usually three reasons or this. Firstly prices were too high and/or secondly, response times were too slow. Or, thirdly, our demands for particular style and quality were too onerous.

Contracts for switching gear and phones went to Leeds based businesses and furniture contracts went to London based businesses. Competition, particularly services competion, is not significant enough close to home, here in Newcastle.

The impact on innovation follows on from the impact on competition. In research for the then Scottish Development Agency, we found that firms in the South East took up innovation faster than firms in Scotland. We attributed this to the impact of firm density. It will always be the case that fewer people and businesses will mean less innovation, but this was something in addition. There is less incentive to take up new ways of doing things.

Business density has a partner in the business birth rate / business death rate.

Let us assume two hypothetical locations – ‘dense’ and ‘sparse’. Dense houses 200 businesses and Sparse houses 150. Both however have the same business birth rate of 10%. Next year, Dense will therefore house 220 businesses and Sparse will house 165.

What began as a business stock difference of 50, has grown to 55. The rich really do get richer, while the poor really do get poorer.

If low business density has an impact on competition and innovation, it follows that productivity will be lower also. We have to increase the number of businesses.

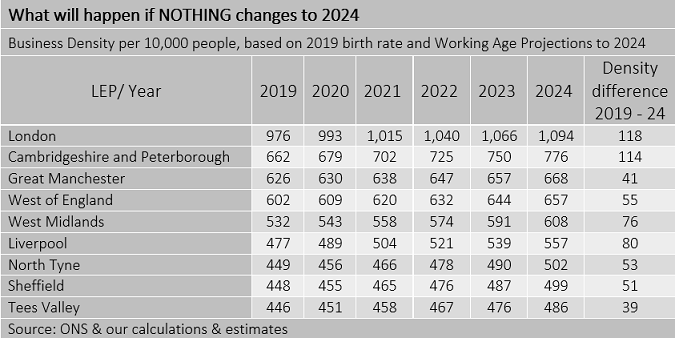

This is a ‘thought experiment’ that starts with 2019 data – but of course the principle applies if we were to start today.

Today, Newcastle has a business density of 432 businesses per 10,000 people. North Tyne (the area covered by the Mayor) has a business density of 449 per 10,000 people. The business birth rate across North Tyne varies between 11% and 15%. If birth rates stay the same until 2024, and we assume working age projections from ONS, then business density for North Tyne will increase to 502 businesses per 10,000 people.

This is shown in the Table.

But of course, everywhere else is changing also. The table shows how a stable business birth rate interacts with ONS projections for the working age population to 2024. The table indicates the degree to which, over this 5/6 year period, places will catch up with one another. For example, in North Tyne, we’ll have 53 more businesses per 10,000 people; Greater Manchester will have 41 more. So we’ll have caught up a bit with Manchester. But we will have lost our advantage over Liverpool because they will have 80 more businesses per 10,000 people in 2024 than they had in 2019.

More than this, the table emphasises the significant differences between the South East and everywhere else that I indicated at the beginning.

I have argued in an earlier post that we should not be picking winners. There are two reasons for this. Firstly, it’s too hard. Secondly, attempting to pick winners consumes a lot of resource. Advisers, bankers, financiers, all combining skills to deliver some kind of alchemy.

What we should do instead is let the market pick our winners.

We’d be better off throwing (I use the word advisedly) a ‘start and run a business’ education pack to anyone who wants to start a business. It doesn’t matter whether it’s a haidresser or a search engine to rival Google. More people running businesses means more role models for others to do the same; more businesses means more competiton; more competition means innovation; more businesses will enhance productivity. More productivity means greater GDP. And so on. This is the virtuous circle we need.

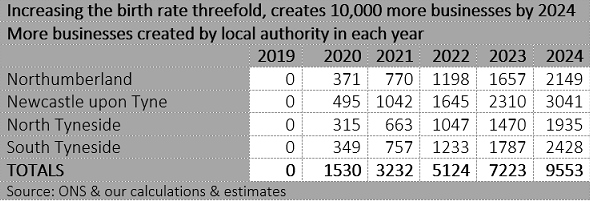

Let’s imagine that in North Tyne, we add 10,000 MORE businesses by 2024. Let’s also imagine that the other places in the UK identified in the table above, pursue the growth trajectory I show there – they do not change their current trajectory. IF we added 10,000 businesses in North Tyne, we’d shoot up the table to within a whisker of Greater Manchester.

Let’s imagine that in North Tyne, we add 10,000 MORE businesses by 2024. Let’s also imagine that the other places in the UK identified in the table above, pursue the growth trajectory I show there – they do not change their current trajectory. IF we added 10,000 businesses in North Tyne, we’d shoot up the table to within a whisker of Greater Manchester.

And let’s not forget how those 10,000 businesses to 2024 might be delivered. Firstly, it’s not 2,000 a year and secondly, the effort is distributed across four local authorities.

It is not 2,000 a year because it builds up – this is the virtuous circle effect. The final table below shows (a) how the effect accumulates over the years to 2024 and (b) how the heavy lifting would be distributed across local authorities.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >To grow a business, someone has firstly to start one and then run one. Admittedly the same person does not have both to start a business and run it, but for the moment let us assume that this is one person and that her name is Olivia1The most popular girl’s name in Britain 2019. . Olivia is interested in starting and growing a tech business.

There are two sources which inform our understanding of this. After that, we can consider the impact of these things on new business creation.

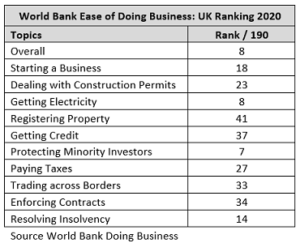

The 2 data sources that tell us about the environment for starting and running a business to grow it, are the World Bank Doing Business project and the Global Entrepreneurship Monitor project. The former offers a macro view, the latter a micro view.

The WB Doing Business database captures 190 countries and ranks the ease of doing business across 10 variables. The table shows the summary results for the UK. The overall rank of 8 for the UK is very high. It is easy to ‘do business’ in the UK.

The WB Doing Business database captures 190 countries and ranks the ease of doing business across 10 variables. The table shows the summary results for the UK. The overall rank of 8 for the UK is very high. It is easy to ‘do business’ in the UK.

Note that the variables that contribute to this overall rank cover a lot of ground. They include for example that, in some countries, it is very difficult to access electricity. Also, in some countries, Olivia would find it hard because she’s a woman.

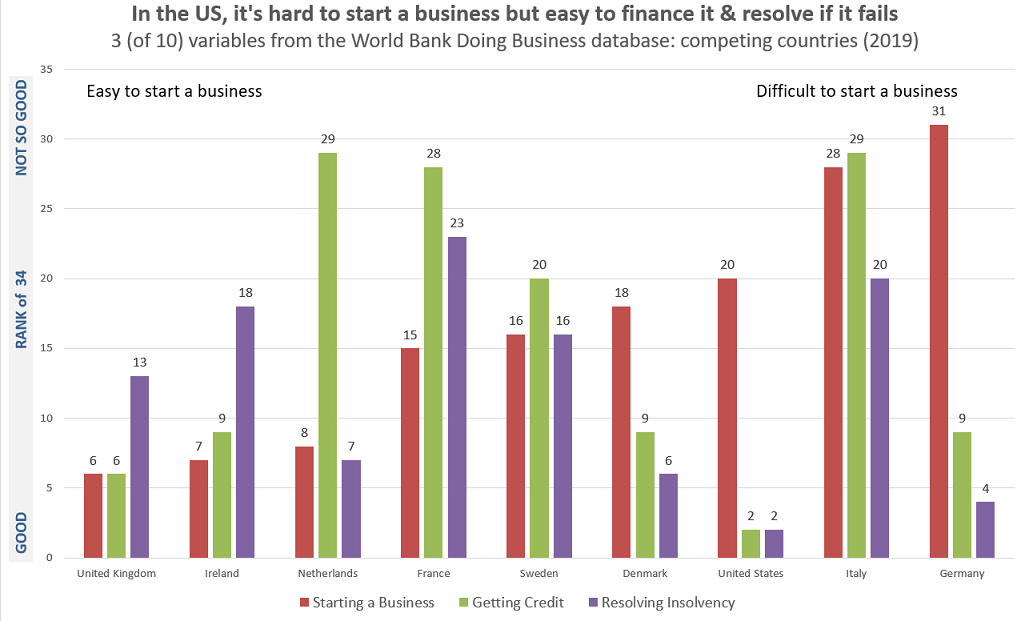

There are 3 World Bank variables that are particularly interesting for Olivia. They are: (a) starting a Business, (b) Getting Credit and (c) Resolving Insolvency.

There are 3 World Bank variables that are particularly interesting for Olivia. They are: (a) starting a Business, (b) Getting Credit and (c) Resolving Insolvency.

For Olivia to grow her business, I suggest we need to look at an additional variable. I discuss that variable below.

This chart shows these 3 variables for a number of competitor countries. The ranking here is different. The ranking here is based only on the 34 members of OECD, not all 190 countries in the full World Bank Doing Business Database.

The chart shows just how different is the US from these comparison countries. My interpretation is summed up in the chart headline. In the USA (to which we should aspire in terms of their ability to grow businesses), it is hard to start a business, but much easier to grow it by accessing credit, and much easier to close it, should it run into trouble.

Resolving insolvency easily is important. Things go wrong and when they do, they should be sorted out quickly. Speedy resolution means that key players can move on, learn from mistakes, and start again. Many have pointed out that, in the UK, there is a degree of shame being associated with a failed business, while in the US it is viewed as a learning experience, a stepping stone, a rite of passage. The ease with which insolvency is resolved in the US is an aspect of this.

Subtly, the fear of insolvency affects entrprepreneurs’ attitude to risk. Growing a business involves taking risks. While I do not believe that people take reckless risk, it is obvious that reducing the ‘costs’ of insolvency is likely to enhance attitude to risk.

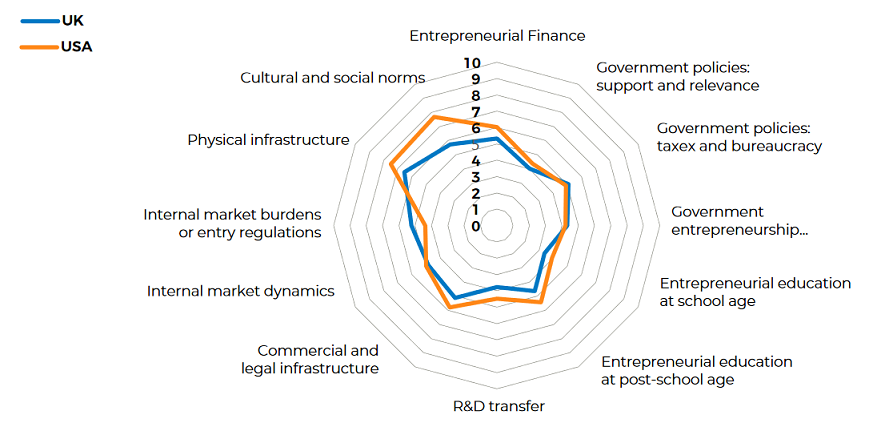

Global Entrepreneurship Monitor has been reporting annually since 1999. The 2019 report covers 50 countries. Each country has its own research team and produces its own report to a global template and standard.

GEM has a measure called ‘Total Early Stage Entrpreneurship Activity’ (TEA) which is the combination of two measures. Measure 1 is ‘nascent entrepreneurs’.

These are individuals who commit resources, such as time or money, to starting a business. To qualify as a nascent entrepreneur, the business must not have been paying wages for more than three months. Measure 2 is ‘new business owner-managers’. These are businesses which have been paying income, such as salaries or drawings, for more than three, but not more than forty-two, months. More detail on the methodology can be found in the UK 2019 report.

TEA for the UK in 2019 was 9.9% which is close to half the US rate of 17.4%. Although I’m not a fan of spider diagrams, this one shows the key differences between the US and UK which go towards explaining this difference. A score closer to 10 is better.

A look at the variables suggest that there is little local economies can do in the UK to address these differences. However, there is one exception to this – a variable that can be addresssed locally. And a second over which a degree of influence is possible. These are the two variables to do with ‘entrpreneurial education’. One of these looks at entrepreneurial education in schools. The other looks at entrepreneurial education post school.

Recently, I have sat in on virtual meetings and also seen commentary on social media which refer to the ‘digital jobs market’ in Newcastle. Apparently, a large proportion of all advertised jobs are tech related. Also, I have heard many references to initiatives designed to enhance the ‘careers’ of young people in technology.

But enhancing her ‘career prospects’ in IT, is not what Olivia wants. She doesn’t want a career in IT. Olivia wants to start and grow an IT business. Olivia wants to offer careers in IT.

For Olivia, this is a problem. She knows (because she’s read the GEM Report on Britain), that entrepreneurial education is important, but she struggles to find it in Newcastle. Olivia has looked at the syllabuses at Newcastle schools including Newcastle’s University Technical College and has come away disappointed.

Olivia was particularly disheartened by two comments on the UTC why we’re different page.

One comment told Olivia that she’d be wearing ‘business attire’ – which is not the image Olivia has of a tech entrepreneur. The other comment told Olivia that she would be occupied during ‘9-5 working hours’. And again, this does not match the picture Olivia has of life as a tech entrepreneur.

So, based on real data comparing us with other countries, it is possible to identify things we can do to help Newcastle build more businesses and bigger businesses. However, it is important also to recognise that nothing we do will deliver results fast. Some of the things that the US does, and to which I referred in another post (like SBIR), have been in place for many years. The UK, having implemented SBIR badly, abandoned it. Policies like enhancing entrepreneurial education need commitment and review continuously.

It is possible for Newcastle to get great. It can only do that based on understaning its position in the world. That understanding is ONLY possible by analysing data.

Policies are no good unless they are monitored. What is our starting point? How does Newcastle’s business demography stack up and what might be sensible targets for say 5 years? I discuss this here.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

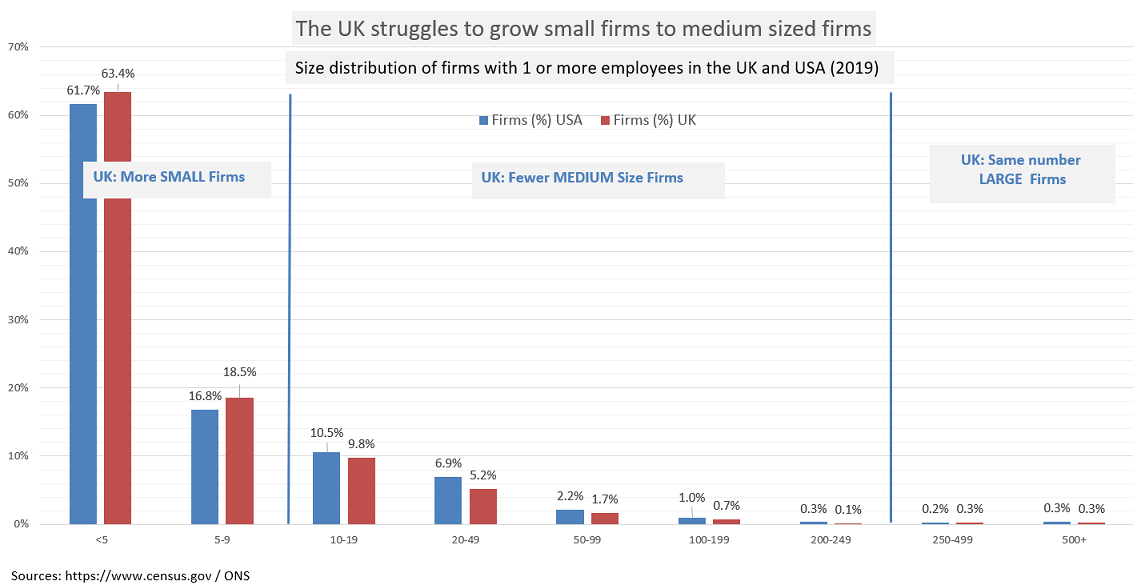

Read More >Scaling up a small UK business is an issue. Many have referred to this. The chart shows it to be true. Growing a small business to be a medium one is difficult.

To address this, the UK has established the The Scale Up Institute. The mere establishment of this body lends weight to the problem and at the same time effectively downplays the importance of new business starts. In a piece in the Financial Times, John Mullins, an Associate Professor at London Business School is quoted saying:

“A common mistake is to focus on simply increasing the number of start-ups. Policy should instead be directed towards “scale-up” companies, many of which will already be trading but need to change their business model to find a more growth-oriented niche. Encouraging start-ups, given the churn that will inevitably occur among them, is the wrong place for government support. A wiser course would be to support growth in companies that are ready to scale up”

To which I would say:

Therefore, I don’t agree that this is an ‘either / or’ for Government policy. It’s both.

More than this, in arguing for us to direct support towards businesses that are ‘ready’ to scale up, we are lead to trying to pick winners. We first tried to pick winners for business support during Margaret Thatcher’s premiership. The UK returns to this theme regularly without any evidence that it is possible. It is true that the Scale Up Institute is saying that it is using AI to ‘pick winners’ so things may have changed. We will see.

All I would say is that in the USA, the most successful economy we seek to emulate, there are NO federal or State programmes that could be described as based on ‘picking winners’.

Therefore, start up and scale up are both important. How might we address deficincies in both?

The commentary around growing business is heavily focused on the failings of the firms themselves. Management is insufficiently skilled to grow the business. To remedy this, we have training and development programmes to ‘scale up’ small firms to large ones.

Of course it is possible that our entrepreneurs do lack the skills to grow businesses, although I am not sure how this could be established with certainty. However, the evidence does suggest that there is indeed an issue to do with ‘entrepreneurship education’ which I cover here.

There is an equally plausible explanation why the UK struggles to grow its small businesses by comparison with the US. This explanation is based on two things that distinguish the US and UK. Firstly, the US market is around 5.5 times that of the UK. This means not only that there are more people to sell to, but it also means that prices can be lower. The price advantage enjoyed in the US market can easily be extended to smaller, overseas markets creating a highly virtuous circle.

The business-to-business market is similarly distinguished.

The chart above does not capture firms with zero employees. In the UK, there are 4.6 million businesses with no employees. In the US, there are 24.8 million. Again 5.5 times as many. In total, (i.e. this number plus the numbers from the chart), there are 30.4 million businesses in the US; in the UK, there are 4.9 million.

This means that an SME developing business software has 30 million sales opportunities in the US and only 6 million in the UK. Pursuit of 0.1% of the business market in the US = 30,000 targets; in the UK = 6,000 targets. And so on.

This is a big deal. Speaking as someone who springs from a company that develops business software, I know that the US dominates almost every niche, with products that are cheaper than home grown examples. Having said that, I am intrigued that Australia and New Zealand seem to punch above their weight. Xero and Atlassian are examples.

Our membership of the EU should have addressed the market size issue. The EU market is even larger than that of the US. However, our 40 year membership of the EU has not obviously addressed the issue. This suggests the second of my speculative guesses about why the UK does not grow its small businesses. This is the British (losing) struggle with foreign languages. Not only does the US have 30 million business to business sales targets, those targets also all speak English. Selling to 0.1% of them in the US, delivers a financial platform to develop foreign language versions of whatever it is being sold. Yet another virtuous circle.

While I recognise that our membership of the EU single market may not have impacted the chart above, it is surely the case that exiting the single market will not have helped.

But for the moment, we have three possible explanations why the UK does not grow its small businesses: our entrepreneurs are not skilled enough, the UK market is not big enough and we expect our customers to speak English more than we should.

The first of these explanations, that our entrepreneurs are insufficiently skilled, is supported by the findings of the Global Entrpreneuship Monitor. They are particularly pertinent to Newcastle and the North East. This is discussed here.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >When they are right, why are economists so easily ignored? Simon Wren Lewis, a macro-economist wrote a recent, good, blog on this. For those of us who have worked with regional economics, the problem is further complicated because the data is messy. But, ‘levelling up’ regional economies requires us to grapple with these difficulties, all the while remembering that we’ve been here before.

For example, not too long ago, most of us accepted that small firms create jobs and big firms lose them. That conclusion is now mediated by some who say that the quality of the created jobs is poor and low skilled. Or, that we do not need jobs in more firms, we need more jobs in fewer, high growth firms.

The latter is a very seductive argument for regional players. The PR that comes with association with a high growth business is attractive. And in a small regional economy (like that of Newcastle and its neighbours) it is easy for a very small number of growing business to assume significant status.

So do we need more firms? Or better firms?

In the North East, what are the features the regional economy that need ‘levelling up’ and what do we do to make it happen?

Along with others, I would argue that GDP is the key metric that would indicate that ‘levelling up’ has been succesful. If we achieve higher GDP, almost everything else follows. So what needs to happen to raise regional GDP?

In the period of the last Labour government, a lot of money slushed around to deliver regional growth. Agencies were created and research funded to answer what, at the time, appeared to be useful questions.

I think that a lot of that research was good, empirically robust and policy driven. Also, a significant number of good ideas were copied from the US.

However, the initiatives that flowed from the research were often badly implemented or non-existent. The project management was terrible.

Where ideas were copied from the US, there was little attempt to understand why they worked on the ground in America. What was it about the particular US environment that made them work?. 1Two initiatives which are examples of this are SBIR (the Small Business Innovation Research initiative) and BIDs (Business Improvement Districts). The former is long abandoned in the UK, but going strong still in the US; the latter is going both here and in the US, but rather more succesfully in the US. There is more detail about why these initiatives were poorly implemented in the UK here.

And at the end of this golden age of economic development initiatives, we’re still talking about the need to ‘level up’.

Unlike the ‘golden age’, the last decade has witnessed an almost complete absence of notable, centrally driven, regional economic research. Picking the golden nuggets from the golden age, I would argue for the following, ‘truths’ :

In this post and others which follow, I discuss these point with a focus on the North East with an attempt to use official data (ONS / NOMIS).

I am not reviewing the academic work on all of this. I hope I manage to inject a measure of ‘it’s obvious isn’t it’ without referencing the literature.

I am not going to say much about this. The initial research was conducted by David Birch at MIT. In 1979 he published The Job Creation Process, in which he showed that most new jobs in the US are created by small companies. This study caught the attention of politicians at home and abroad. Birch’s work, although criticised, is considered groundbreaking because it opened the study of small businesses, which had been disregarded by economists before this.

I am not going to say much about this. The initial research was conducted by David Birch at MIT. In 1979 he published The Job Creation Process, in which he showed that most new jobs in the US are created by small companies. This study caught the attention of politicians at home and abroad. Birch’s work, although criticised, is considered groundbreaking because it opened the study of small businesses, which had been disregarded by economists before this.

The research to see if what Birch had found in the US, applied in the UK, was funded by the Department of Education and undertaken by Trends Business Research (confession: this is a company which I founded). More recently, but still more than 10 years ago, the Department of Business (BEIS) commissioned a team at Aston University to look again – and the core finding that small firms create jobs, holds true.

When I first got involved with these findings, like many, I was initially surprised by them. Surely, big firms must turn in big job creation alongside big revenue. But a few moments reflection tells us that the finding is accurate. The news we read is of big firms delivering real, significant job losses and the number of small firms an any economy far outweighs the number of big ones. Common sense affirms the core finding. And although I am not reviewing the literature, I will say (because I know it to be true) that Trends Business Research went to the most enormous trouble to confirm the data.

This is not to say that other points about the quality of the jobs or the regional disparities or the sector distribution are not accurate. It is merely to say that job creation comes from small firms.

With that thought, the bigger question is why does the UK struggle to grow firms? What is the size of the problem? I discuss this in this post.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >How must offices in a post Covid-19 world adapt to play their part in restoring vibrant life to our city centres? There are 5 lessons to learn.

In an earlier post, I spoke about what we’d like to see to encourage businesses and people back to Newcastle City Centre and its close neighbourhoods. Most of the things I spoke about are not within our gift. However, we recognise that businesses like ours – responsible for office space – have a part to play. How must The Racquets Court begin thinking big about smaller offices, to meet the changing demand for space.

In the past 12 months, we (and most of the planet) have learned how to work from home.

We know what we like about it and what we don’t. We know what we miss and what we do not. We’ve solved some problems and not others.

The genie is out of the bottle. It will not be put back.

We are not certain what all of these lessons are, but these are some that we are working with. We must:

The evidence suggests that, where home is comfortable, people enjoy working there. That phrase ‘where home is comfortable’ however is a big one.

There is an obvious connection between how well off someone is and the degree to which they find working at home comfortable. More than this, the better paid will find it easier to afford the additional costs of working at home. Although homeworkers save on travel (and on clothes that are worn below the waist), outside the South East, this may not compensate for the greater costs incurred for utilities.

There are other issues. ‘Before Covid-19’, home was big enough, now it is not. The desk chair used for brief periods before Covid-19 was OK; sitting on it now for hours at a time, it’s killing my back. Before Covid-19, the table was OK for brief periods of work; as a desk, the table is too small. And ‘my table’ has not before been used so extensively for work; my table is my metaphor for the difficulty of separating home from work. Where does one stop and the other start? Before Covid-19, this was relatively easy to distinguish; today it is much harder.

Connectivity? OK for my personal use; Zooming and Teamsing all day is entirely different. And my partner is on it too – it won’t cope.

Microsoft has largely found itself missing out on the plethora of slang associated with the harms associated with video conferencing. We have ‘Zoom Gloom’ and ‘Zoom Fatigue’. The slang does however mask real concerns about the psychological impact of the exccessive use of this technology.

So we should assume that employers who care about their people will wish to reduce the use of Zoom and Teams by bringing them back into an office – at least for part of the week.

We have to be comfy. We’re not ‘home’ but we can be a great alternative. You will not get a bad back sitting at your desk (because the chairs have won design awards in Germany and the USA). The desks are amply sized, screened and with nifty pull away tops to hide the wires. They are made in Yorkshire. The office will be quiet because the carpet is designed to insulate you from office noise.

The coffee won’t run out, because it’s locally sourced and delivered. When the building is full, you’ll be able to reach into the fruit bowl and grab an orange or an apple, sourced from Grainger Market. You’ll never have to wait for the kettle to boil or for the tap to run cold because boiling and chilled water is on tap. And your space will be clean – because we clean it every night. (And we employ our own cleaners – on excellent terms and conditions).

These luxury features have guided us from the beginning; we have always wanted to be thinking big about smaller offices.

You will probably not want space every day of the week. We will therefore offer you space when you need it. If you need desk space for only 0ne or two days a week – then we will make that possible. If you need one desk one week and two every other week – we’ll accomodate that too. If you need to meet others in the middle of the night – well, that OK because the building is 24/7.

We recognise also that this way of working is unlikely to reduce the Zoom or Teams load. This is because not all of your people will be together at the same time. So we will make our meeting spaces more flexibly available. Before Covid-19, meeting room were bookable for a minimum of half day. We will reduce this to 2 hours for those outside The Racquets Court; for members, we will reduce this to one hour.

We recognise also that this way of working is unlikely to reduce the Zoom or Teams load. This is because not all of your people will be together at the same time. So we will make our meeting spaces more flexibly available. Before Covid-19, meeting room were bookable for a minimum of half day. We will reduce this to 2 hours for those outside The Racquets Court; for members, we will reduce this to one hour.

And of course, you do not have to worry about connectivity. The Racquets Court is one of the very few buildings connected to Stellium’s Metro Network. We have a Gigabit carrier and 200 Mb up AND down. Every desk has a wired connection and there are 3 wireless networks in the building. If you need extra security, then we can offer your own connectivity the Metro Network.

Currently, desks are socially distanced; we have reduced the capacity of our cafe area.

We have installed a facial recognition, no touch, temperature scanner. We anticipate that everyone entering The Racquets Court will wish to ‘scan in’.

There is a hand sanitisation station at the entrance to the building and all sinks are stocked with Arran Aromatics luxury hand wash and hand cream. Regular handwashing and sanitising is drying out our hands. It is very important therefore to moisturise them.

Additionally, The Racquets Court has a sophisticated air circulation system. It does not have air conditioning. The system continuously draws fresh, filtered air into the building and pushes out the air from inside.  Therefore, you can feel confident that the air you breathe is as fresh as possible and filtered.

Therefore, you can feel confident that the air you breathe is as fresh as possible and filtered.

Our system is also more environmentally friendly than air conditioning, helping to protect our planet as well as our people.

The Racquets Court also has a self-opening glass roof for maximum fresh air. And of course, it has rain sensors so it closes automatically when the weather turns.

Many of us are avoiding public transport and cycling. Newcastle City Council is promoting this of course with more cycle lanes. The Racquets Court has secure bike storage. And there are luxury showers to freshen up (Arran Aromatics toiletries provided).

If you are running a business, and you’ve downsized your office needs, we assume that you will wish to devote resource towards making your people feel as though their home / office balance works in their favour. This is about your business thinking big about smaller offices.

If you can get it right, if your people feel that they can get the best of both worlds (comfort, ease, frustration-free, hygiene factors satisfied), then employee satisfaction will be high and productivity will increase.

And the cost to you is predictable; there will NO additional costs except for those you ask for such as a meeting room for an hour or two.

If you are an employee, then going to the office should be an appropriate alternative for everything that working from home might offer. And perhaps that should include the odd additional trinket that you might not get at home. This might capture some of the things mentioned above, but also easy access to John Lewis, Marks & Spencer and Fenwick, a drink after work in a City Centre pub, followed by a trip to the cinema or theatre.

This is what we mean by thinking big about smaller offices

In my last post on this subject, I talked about Newcastle’s ‘bit’ – those things over which we have no control which make our City attractive. This post has been about our ‘bit’

Our ‘bit’ is the offer of luxurious office space in the centre of our City which people will WANT to work in. The future appears to be that many of us will wish to combine working from home and at the office; we believe that The Racquets Court can be ‘the offfice’ that makes this combination work to the benefit of businesses and the people who work in them.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >The Racquets Court is dependent on vibrant life returning to Newcastle. And vibrant life in the City depends on workplaces like The Racquets Court. We’re inter-dependent. This post is about making Newcastle attractive to business. If we can do this, the people of Newcastle, and around, will return – in droves.

What must we (the owners of The Racquets Court) do, (our bit) and what must ‘the City’ do, (its bit)? This post is about the latter; we discuss the former here.

For close to a year, there has been a debate about lockdown choices. Should we prioritise health or the economy? Our position is that this is not a ‘choice’. We prioritise health because unless our population is healthy, they will not be working, buying goods and services, stimulating demand. The health of our people is the pre-condition to a healthy economy.

Some may argue that investing in our City is a ‘choice’. In other words, we can choose between prioritising resource allocation to our communities most in need, and investing in making Newcastle attractive to business. However, like the Covid-19 example, this is not a choice. Unless Newcastle is attractive to business, those most in need will continue to suffer joblessness and deprivation. Businesses that are attracted to Newcastle or are started here, create jobs which are a pre-condition for an end to deprivation.

Restoring life to Newcastle is about reimagining the extensive literature on what makes locations attractive to businesses. This is not new material; it has been around a long time. We must remember and adapt it to the current / post Covid-19 situation we face.

Location attractiveness to businesses – those who run them and work in them is about four features:

In spite of evidence that shows that, for entrepreneurs, theatres, galleries, museums are greater attractors than beaches and countryside, the North East seems wedded to promoting the latter over the former. Perhaps this explains why Darlington has attracted the Treasury rather than Newcastle – an odd decision which may incite insurrection amongst the Mandarins.

For Newcastle, it must be a priority to open our culture venues as soon as we can. They must not be starved of support; their role is crucial.

People will continue to be nervous of public transport for some time. How might we facilitate access? Perhaps the restrictions on some parking might be eased? Perhaps city fringe spaces might be opened? For example, the space traditionally used for the Hoppings on the Town Moor might be used with people completing the journey on foot. How many other cities in the UK have such a potential facility so close to the City centre?

I am not of course suggesting this as a permanent facility – merely a temporary one until a semblance of normality is resumed.

It’s very good news indeed to see that the City is to invest in its Centre. I have occasionally been dismayed by previous efforts in the City which have featured copious quantities of astroturf and planting and plant containers that are aesthetically challenged – so please let this happen to deliver a ‘wow effect’.

But it’s not just the City Centre. Gosforth is a key residential attractor for entrepreneurs and others thinking about re-locating to Newcastle. Gosforth High Street is currently a mess of largely filthy red and white poles delineating cycle lanes, with the white patches peeling off many of them. This is not a plea for the removal of cycle lanes. It is a plea to make them look good.

To deploy a cliche … last but not least. Those that know my background will be unsurprised to see me talk about clusters. I led the UK’s whole economy cluster mapping project in 2001; I remain persuaded that the concept is powerful. It is surprising just how much of what we said 20 years ago, retains its currency.

For businesses like ours (data technology – ish), proximity to Newcastle University is a great example of the cluster phenomenon. However, the relationship of our business to others, close by, is less obvious. I have no idea what clusters there are – and I am not persuaded that others do.

Our own City of London is an obvious blueprint. The City takes in all financial services, City University, specialist printing (financial services is THE biggest user of print services) and so on. Post Brexit – who knows?

Outside the UK, the clothing cluster in Los Angeles is a wonderful exemplar. The cluster captures masses of manufacturers right there in central LA, the Fashion Institute of Design and Merchandising (FIDM) and California Mart, where buyers from across the US can easily visit hundreds (yes hundreds) of small clothing designers.

I recall discussing the strategy that gave rise to the re-imagined and commercially successful fashion infustry in Los Angeles (with the LA Development Corporation). My overwhelming impression was the clarity with which the strategy was articulated, based as it was on a solid research base. The LA cluster is now bigger and more successful than that in New York. It has given rise to brands like Diesel and American Apparel as well as clothing tech businesses that challenge the traditional hegemony of France and Germany.

Both of these are examples of clusters based on markets (finance and clothing). Today, we’re more likely to see clusters defined by a technology – ‘digital’ for example.

I find it difficult to identify the glue that might bind businesses together simply because they use similar tech. Certainly, the most recent work on clusters is remarkably devoid of a market focus. A 2018 BEIS study uses some nifty maths to identify clusters, but I don’t see what use the analysis is.

For example, this study identifies the second largest advertising cluster in the UK to be centred on Manchester (my team found the same in 2001 – industrial structures change slowly). However, the study evinces no curiousity about why it’s located there.

The answer is to with the fact that Manchester was the home of the original catalogue industry (Grattan for example) that sprung out of the clothing businesses based in the North West – the precursor of online apparel. 1 THIS IS WHAT WE SAID IN 2001: Perhaps associated with both textiles and household goods is the region’s major strength in mail order retailing. Its size, degree of geographic concentration, links to industries such as market research, advertising and packaging and its role as a distribution channel for consumer and household goods, suggests that mail order might be seen as a significant regional cluster in its own right. In this context, it is worth emphasising that the industry is not dissimilar in many ways to the emerging dot.com industries.

And from the embers of what was there, other things spring up. Alongside Misguided, there is Boohoo, Pretty Little Things, Matalan and others. Supporting them is the textiles department of Manchester University and those other industries (advertising and so on), that we identified in 2001. They are all thriving and adapting in a digital age.

Having a market oriented understanding of clusters enables strategies to prevent clusters unravelling, or stimulating appropriate responses if that unravelling can’t be stopped.

For the moment, suffice to say that the evolving industrial structure of Newcastle has never been more important. I don’t detect a strategy for it, but if vibrancy is going to be restored to our city, then we need one.

As a business resident in Newcastle, I am not wholly familiar with the parties to all of this. I think my comments take in the City itself, NE1 (the Business Improvement District for central Newcastle), The Freemen of Newcastle (who own the Town Moor), bus operators and so on.

This is important for us. We’d be prepared to increase our NE1 levy to contribute. I recognise this is a team effort – we want to be in the team …..

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >If you were to use our headline as a search term, you’d find very little to answer the question that’s implied. This, from Zoopla, is one of the better pieces – at the least it refers to things like energy costs.

However, if you agree a conventional lease on office space, you’ll perhaps be surprised to discover that the most expensive thing you contract for is likely to be your cleaning. The Zoopla piece does not mention it and it’s never highlighted – perhaps because ‘dirt’ is not something we want to think about too actively. Or perhaps it’s because cleaning contracts conjure a picture of poorly paid, often exploited, usually women employees.

However, when researching this broad area for our investment in The Racquets Court, it became clear that cleaning is either first or second on the sorted list of costs associated with occupying an office. The only cost that cleaning might compete with is connectivity – I’ll come back to that.

With all of this in mind, let’s look at the TRUE cost of office occupation – both the tangibles and the intangibles.

In what follows, we’ve assumed an office space of 1,866 square feet – coincidentally, the space on the first floor of The Racquets Court.

The unskilled nature of cleaning leads to exploitation and cut-throat competition amongst companies. The following breakdown is on a cleaning company’s website; I’ve updated the salary cost to reflect the current minimum wage and assumed 2 hours to per day for a space that houses around 20 people. This will include things like emptying waste paper bins, keeping paper goods topped up and so on.

| Hours | Days | Per week | Per annum | |

| Daily | 2 | 5 | 10 | |

| Deep clean | 1 | 1 | 1 | |

| 11 | ||||

| Pay per hour | £8.21 | £90.31 | £4,696.12 | |

| On costs | 15% | £103.86 | £5,400.54 | |

| Materials | £9.00 | £468.00 | ||

| Company service charge | £800.00 | |||

| TOTAL | £6,668.54 |

So, around £7,000 per annum or £3.75 psf. In The Racquets Court, we’ve decided to employ our own cleaning people. They are paid £10 per hour and their terms and conditions are the same as others we employ. Broadly speaking, we’ve chosen to apply the margin that a cleaning company might enjoy to the package enjoyed by the cleaners themselves. This does represent a management overhead for us, but one that we think is right.

Usually around £6 psf in Newcastle, this will cover things like cleaning and lighting common areas, the rubbish disposal contract, insurance and so on.

OK, you may not choose to provide this, but if you do, you’ll find it costing around £5 pcm per employee to which must be added the overhead associated with providing decent coffee making machinery. This will total around £0.90 psf.

One of the more difficult to forecast but for a business employing around 20, the total power bill is around £6,500 per annum. See here for some detail on that. In our example, power will cost around £3.50 psf.

In Newcastle, rates add between £7.50 – £8.00 psf. So, let’s assume, £7.50

The main costs here are set-up and ongoing. Let’s assume a modest £500 per annum or £0.30 psf.

The Racquets Court connectivity has been well documented. We have a gigabit bearer which is set to deliver 200Mb upload and download. Of course, we can scale beyond this if required. Achieving this routinely with providers (if it can be achieved at all) would require a leased line. There are many providers but this one is representative. The cost is around £300 pcm for a 36-month contract. However, this does not capture the additional costs involved (e.g. firewall). Conservatively, we’d estimate the costs over 36 months to average around £,6,500 per annum or £3.50 psf. For those interested, this is an informative thread on the subject.

Yes, things go wrong. The gas meter reading is weird; the coffee hasn’t turned up for the coffee machine; the maintenance contract on the leased line isn’t delivering; why are those calls being charged for on the phone invoice. And there are around 100 invoices per annum to pay on the maintenance and management of office space for around 20 people. We estimate that this requires around 15% of a person’s time (a bit less than a day per week). This is NOT a simple clerical task – dealing with suppliers who are business critical requires a degree of skill. We assume a total salary bill for such a person (including on costs) to be £25,000 per annum. 15% of this is £3,750 or £2.00 psf.

If we add these costs, we come to £27.45 psf – the sum to be added to the rent psf.

The Racquets Court fit out is very high quality and includes high specification meeting room facilities. This site shows that furniture etc will cost between £1000 and £2,500 per person. The Racquets Court is towards the top end of this. Let’s assume the most basic provision – for around 20 people, this represents a cost of around £25,000 to include meeting room facilities. If we assume depreciation over 5 years, this is £5,000 pa or £2.70 psf.

Cabling for connectivity also represents a one-off cost – obviously written off over the life of the occupancy. We’d estimate Cat6 cabling for around 20 people to cost around £3,000 or £0.53 psf over a (say) 3-year lease term.

Additionally, there is a fit-out cost – perhaps carpeting, perhaps, kitchen equipment, perhaps a wall or two. Knight Frank estimates an allowance of £30 psf for this – if it’s necessary.

Representing both a tangible cost and an intangible cost are ‘dilapidations’ – restoring your space to the condition in which you found it. This is impossible to forecast but it represents an intangible cost as well as a tangible one because it’s often a hassle and often goes to some kind of arbitration.

There are two very significant intangible costs associated with the occupation of office space.

They are:

… the rent per square foot is usually the least costly element of the occupation of an office space. Add in the other tangible and intangible costs and it is clear that flexible, service led space is an attractive option.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >Newcastle / Gateshead has only one FTSE listed HQ, and we’ve felt privilaged that the core team that built Sage Software’s HQ has joined together again to restore The Racquets Court.

We own and inhabit The Racquets Court and that makes us unusual as building developers. We were told that it’s unusual for developers to be as involved as we were with every detail – to include the coat hooks. We were fussy but not once did the teams at IDP, Tolent or Elliot do anything other than rise to meet our frequent challenges. And the ‘process’ was managed as well as the build itself. This came home to us about half way through the construction …

… we were visited on site by two women responsible for a regional charity. As they were leaving they asked us, in relation to Tolent’s people on site, “are they all like that” . When we asked what they meant, they replied “are they all … nice”. Of course, the answer was “yes” and that was our experience throughout – alongside stunning professionalism. The project finished in the week that it was forecast to finish at the outset. How about that for unusual!

Tolent and IDP and Elliots are local businesses and walking around Newcastle, Tolent’s brand is found frequently. But – and this may be the crucial variable – their market is national and perhaps it’s this that makes them competitive and productive.

The Newcastle / Gateshead market is a small one. Indeed, that of the North East as a whole is also. But that’s not the real issue – the real issue is that there simply aren’t that many businesses. In other words, the number of businesses per head of population in the North East is around one-quarter that of London and the South East. Put crudely, there are four times as many interior design businesses in London as there are in the South.

There are a number of implications of this – and some of the most important are not relevant here -but let’s take the implications for a potential customer for any service. If that customer is not aware of this core fact; if that customer travels little in the UK and to the South East not at all, then that customer is very likely to be faced with a price which is high and service which is poor. If local purchasing is ignorant of these facts (and most will be) they are likely not to recognise uncompetitive pricing and will not be demanding customers.

As developers of The Racquets Court, we commissioned relatively few services ourselves. One of the larger services that we did commission is that of connectivity and the bits and bobs associated with it. The core element of that is the Stellium line – upon which we comment elsewhere. Stellium is not a locally owned business and it is by definition global. It behaves that way and service was outstanding.

Stellium only brings a line to the front door – at that point is hits a range of swithches and stuff which distribute connectivity around the building. We initially sought 2 proposals from local businesses. The costs of these were similar – and it seemed to us, rather high.

So we decided to call 2 businesses in Leeds. The first thing to say is that the Leeds conurbation has a signiticant number of IT service businesses from which to choose. The response from each of these businesses was superb – speedy, uncomplicated and friendly. The estimates from these 2 were also suprisingly close to one another. But here’s the thing, these 2 were HALF the cost of the Newcastle based businesses. And that is a very significant sum.

In the end, we had 4 proposals. Each of the 4 offered different switches (3 were Cisco offers), but the fundamental cost differences were down to the offered firewall. We carefully considered the proposals and our key requirements and decided that the expensive firewalls were not appropriate to our needs. We did not consider that local offers quizzed us sufficiently before offering such expensive firewall options.

We did not award the project to the cheapest of the 4 proposals we received.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >We’ve tried hard but it’s really not been easy. Generally, and with some very noteable exceptions, British manufacture and North East business displayed uncompetitive pricing and poor service. Here’s the story.

We know something about industrial clusters, so we knew to take a trip to London. (Paul Miller led the project which mapped UK clusters – here’s the Executive Summary. For more of the study, please contact us).

This is one of the UK’s most dense clusters. All things office interior are to be found in a small patch of Clerkenwell – an area roughly between Angel and Barbican in London.

(All things home furniture are around Tottenham Court Road).

Every British, American and European manufacturer of office interior products has a showroom here alongside consultants and design studios. The area has an annual design event called Clerkenwell Design Week.

We wanted to buy British and to source locally – we were only partially successful.

There are few British manufacturers of high end office furniture. We walked into one of the biggest in Clerkenwell, had a look round and our contact details were noted; 4 days later, we got a call back. We identified in some detail our requirements and then waited. Two weeks after that, we got a call from the Newcastle based agent and we politely offered feedback, once again identified our requirement and once again waited. Nothing happened.

We were also disappointed that UK manufactured products were often significantly more expensive than European competitors.

And then there’s the service and the quality. More on that below.

(We largely achieved ‘buy British AND buy local’ in the restoration and construction of The Racquets Court – that story is here). Our experience of purchased services in the restoration and construction of The Racquets Court – legal, connectivity, internal switches, wifi and so on – is largely good, and that story is here).

We’ve got four seating types in the office: office desk chairs, meeting room chairs, conferences, kitchen chairs and sofas. They come from Germany, Switzerland and Denmark. They have been purchased with lumbar support and comfort in mind.

Our desk chairs are made by Viasit in Germany and the particular model we bought is both innovative and winner of the 2017 Green Product Award. (If you have a product to enter for next year, go here).

The chair’s innovation is in the design of the back, which combines both mesh and fabric. So, it’s a chair that’s good for the user’s back and the environment.

Viasit also make our meeting and conference chairs. The meeting room chairs are a new release from Viasit and was a winning entry on the 2019 German Design Awards. Our Viasit contract was handled in the UK by Office Chairs UK and James Reid there was a delight to deal with.

Our breakout sofas and coffee tables are by Hay – Scandinavian design, from Denmark.

And our kitchen chairs are by Vitra. Vitra is Swiss but with probably the largest Clerkenwell showroom that we stumbled over.

Our UK supplier for Hay and Vitra products was CoExistance and Alex Reddicliffe there was great.

Our desks and meeting tables ARE British! These are designed and made by Flexiform in Yorkshire. Nick Saunders, Flexiform’s Sales and Marketing Director, was really helpful.

Our kitchen tables are Italian, by Plank – again supplied by CoExistance.

Carpeting is by Milliken – a US business which manufactures in the UK. The carpet choice is frankly daunting! And the choice is complicated by the fact that carpet is bought by the decibel. In other words, we had to take a view on the sound insulation necessary in The Racquets Court – not easy in a building that had once been …. well, a racquets court.

Vinyl covering is by Polyflor – and it’s British.

Visitors to The Racquets Court invariably comment on the lighting – it’s ‘architectural’, designed to stand out and largely designed and made by Dorset based Dextra.

Visitors to The Racquets Court invariably comment on the lighting – it’s ‘architectural’, designed to stand out and largely designed and made by Dorset based Dextra.

It’s not usual to find British lighting like this – often it’s Italian. We were thrilled to be able to source lighting from the UK.

Book Now

""

-

3rd March 2026

Remote working isn’t a new thing, but it has grown since the pandemic. Many businesses have embraced remote or hybrid working. This offers more...

Read More >2nd March 2026

We have been Dog Friendly on a Friday for a while now. Why? Well, we like dogs (that’s our director’s dog, Buddy, to the...

Read More >